Business & Technology

UK wealth firm puts aside over £12 million for compensation

Henley-based Courtiers Investment Services’ latest accounts reveal that it has set aside £12,003,171 for the “payment of redress to clients”.

This means setting right, compensating or remedying detriment experienced by a consumer due to a “business failure or negligence”.

READ MORE: UK wealth firm’s £600k office for sale as profits nosedive

This comes after a skilled persons review – an independent investigation – was commissioned at the firm.

Its results statement for the year ending March 2025 said: “The company has undertaken extensive work to identify the clients affected and to calculate the amount payable and a further Skilled Persons review was commissioned to agree the value of the redress.

“The total group provision representing the estimated amount of redress payable at 31 March 2025 amounts to £13,106,203, including interest but net of recoverable VAT.

“Of this sum £12,004,171 is attributable to this company and has been incorporated within these financial statements.”

Based in Hart Street, Henley, City Wire has reported that this represents a significant increase from the £3 million the group had allocated the previous year.

This comes after Courtiers Investment Services voluntarily agreed to a Financial Conduct Authority order to stop taking on new business.

READ MORE: Museum announces major refurb amid wider funding struggles

This agreement happened in 2024 with the firm saying it had done so while it consolidated its acquisitions which included Dorset adviser Snowdon Financial in 2019.

The business did not respond to a request for comment, and it remains unclear when the restrictions will be removed.

In its statement the directors of the firm stated that they consider the financial position of the firm “healthy”.

Gas network company SGN confirmed it had repaired three minor gas leaks and left the site on Monday, August 3, six days earlier than expected.

The leaks were discovered during excavation works last month and contributed to the pushing back of the road’s reopening date, yet again, to September 20.

The completion of the gas mains replacement marked a significant step forward in the wider Oxford Station improvement project, which was originally budgeted at £161 million but is now expected to cost at least £237 million.

The development prompted hopes that Botley Road, closed beneath the rail bridge since April 2023, could reopen earlier than planned.

However, Network Rail has moved to manage expectations, saying the project remains on course to meet its existing target date rather than finish ahead of schedule.

A Network Rail spokesperson said: “We’re pleased that SGN has completed its gas mains replacement work.

“While this is an important milestone, it doesn’t necessarily mean the overall project will finish early as some remaining work is dependent on access to the railway, which we have had to rearrange to enable the replacement of the gas main.

“Our focus remains on meeting our planned deadline of 20 September for reopening Botley Road to traffic.”

While the completion of the gas works removes one of the most recent obstacles facing the scheme, Network Rail says further work under the bridge and around the station is still needed before the route can reopen to traffic.

The club is currently struggling in the summer heat, and has launched a new fundraiser to keep its gymnasts safe.

The club, which is based at Grove House Barn near Warkworth in Banbury, launched the fundraiser so it could buy and install four air conditioning units to keep its space cool.

Currently, the club hopes to raise £7,000 through the appeal so it can buy four 10kW air conditioning units and cover all the installation costs.

So far, the club has raised £380.

Karl Wade, director of Wade Gymnastics, said the club has become “increasingly warm” during the summer months due to the rising temperatures.

READ MORE: Thames Water leakage targets are ‘not realistic’ says boss after pay rise

“Despite our best efforts to keep doorways and shutters open, it becomes very uncomfortable for gymnasts to play and train,” Mr Wade said.

He added: “The safety of our gymnasts and coaches is always our utmost priority.

“Unfortunately, the risk of having to close the business during these hot spells is increasing and we need to have more effective ways of keeping everyone cool.

“An air conditioning system would allow the business to stay open during those extreme hot conditions and continue to provide classes for everyone who attends.”

The gym currently delivers classes seven days a week for around 900 people, which range from toddlers to athletes competing at national level.

The gym club was founded more than four decades ago by Ruth Wade and, for the past 20 years it has been based at its current facility.

SOFIAH NICHOLE SALIVIO

News Editor

Solihull Council has appointed ICS.AI to deliver the first phase of an AI Transformation Discovery programme to examine how artificial intelligence could be used across several resident-facing services.

The 24-week programme will review opportunities in Adult Social Care, Children’s Services, Economy & Infrastructure, and Public Health. It is intended to help the council decide where AI could be used and where future spending should be directed.

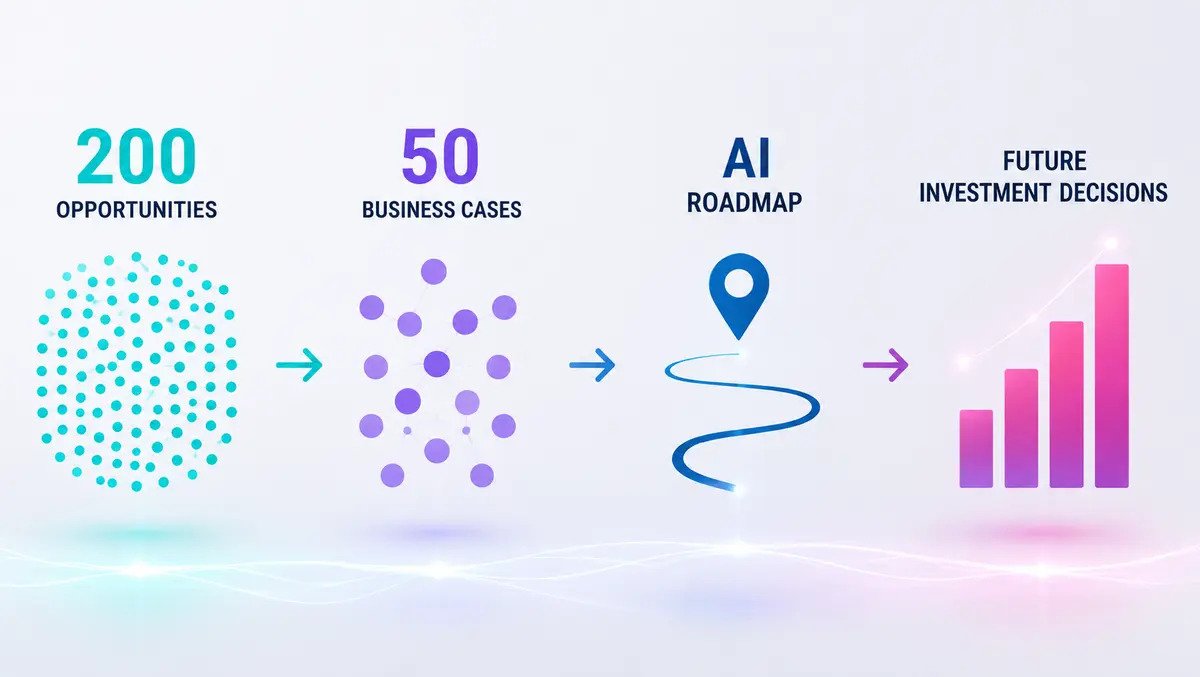

In this first phase, ICS.AI will assess the council’s readiness for AI and identify use cases across the four service areas. The programme is expected to produce a prioritised shortlist of about 200 use cases, including 50 validated from a finance perspective, alongside a longer-term AI Transformation Roadmap.

The work is intended to create an evidence base before any wider implementation decisions are taken. Ethics, privacy, and safeguarding will be considered throughout the assessment process.

Discovery phase

ICS.AI will use its AI Target Operating Model framework to review Solihull’s current position across five dimensions before ranking opportunities. The outputs will be based on council-owned baseline data and reviewed by public sector specialists.

The approach reflects a broader pattern among local authorities exploring AI in service delivery while facing pressure to justify spending and manage risks around data use and public accountability. Councils have also been seeking clearer business cases before committing to larger technology programmes.

Solihull said the discovery exercise would support a measured approach to service modernisation. The authority wants to identify where AI could improve services for residents while also demonstrating value for money.

“We are committed to taking a well-considered and planned approach to modernising the services we provide. By building a strong evidence base for future decisions, this programme will help us understand where the greatest AI opportunities exist. We will then be able to prioritise those improvements that will deliver the greatest benefit for residents, while ensuring full value for the council,” said Councillor Dave Pinwell, Cabinet Portfolio Holder for Resources, Solihull Council.

Public sector focus

ICS.AI said the Solihull engagement builds on work it has carried out with more than 20 public sector organisations using its AI transformation and discovery assessments. Those organisations include Derby City Council.

The company focuses on AI projects for the public sector, where interest has increased as authorities look for ways to manage demand pressures in social care, public health, and other frontline services. At the same time, councils are under scrutiny to show that new technology investments are proportionate and supported by practical evidence.

Dwayne Johnson, Chief Local Government Officer at ICS.AI, said local authorities need stronger justification before committing funds. “Local authorities need confidence that every investment is backed by robust evidence and long-term value for residents. Solihull Council is taking the right approach by starting with a structured discovery programme that builds a clear understanding of priorities before decisions are made. By developing finance-validated business cases and a practical roadmap, the council can be more proactive in the decisions it makes,” he said.

The programme’s initial outputs are expected to give Solihull a ranked view of where AI could be applied across services, the level of organisational readiness, and which projects may warrant further consideration. This first phase is focused on identifying options rather than moving directly into deployment.

For local government leaders, that distinction is becoming increasingly important as councils test AI in areas that affect vulnerable residents and essential public services. In Solihull’s case, the work spans some of the authority’s most visible functions, including care services, children’s provision, public health activity, and parts of local infrastructure planning.

The council aims to use the findings to inform later investment decisions through finance-validated business cases and a practical roadmap for future priorities.

-

Business & Technology3 weeks ago

Business & Technology3 weeks agoHSBC UK & Visa test AI shopping with live payments

-

Business & Technology3 weeks ago

Business & Technology3 weeks agoValarian lands USD $50 million backing for sovereign AI

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoMouser warns against viral hacks to cool overheating phones

-

Oxford News4 weeks ago

Oxford News4 weeks agoNew romantasy bookshop attracts queues of customers

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoSNP & Palantir launch AI tools for SAP transformations

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoKane tops England influencer rankings after Mexico win

-

Traffic & Transport4 weeks ago

Traffic & Transport4 weeks ago‘I felt my spine and body split’: the woman who was hit by a child on a Lime bike – and denied compensation | Ebikes

-

Oxford News4 weeks ago

Oxford News4 weeks agoDWP now checking bank accounts for Universal Credit and Pension Credit