Business & Technology

Platforms, sovereignty and global growth at Cavell Summit Europe

This year’s Cavell Summit Europe provided us with an agenda that reflected the real pressures service providers are now facing today. Senior leaders within the cloud communications ecosystem are now tasked with adapting to structural changes in 2026 and beyond.

What’s key to remember is that these aren’t theoretical futures. Practical shifts are already underway, and the disruption that follows is structural, not cyclical.

Matt Townend’s keynote address established the framework for everything that followed. The focus was on how factors such as pricing pressure, changing buyer behaviour, AI, security, and sovereignty are no longer temporary challenges.

Instead, they form a permanent operating environment for service providers trying to protect margin, while continuing to grow.

It resonates with the wider conversations being held in the wider service provider space. The reality is that nobody is asking whether the market is changing. Now, it’s how to effectively adapt to conditions without increasing complexity or risk.

Global platforms and marketplaces are also reshaping buying journeys. There’s now extra attention being paid to these areas, especially as communications services are no longer sold in isolation. Solutions are now being embedded into CRM, CX, and productivity ecosystems.

Platforms, such as HubSpot, are beginning to act as commercial entry points for telco services. Salesforce’s own move into digitally purchased contact centre capabilities also signals a wider shift in how voice and CX are both packaged and consumed.

What does this mean for service providers? It’s a material change, where customers increasingly expect communications to ‘fit’ into existing platforms. Buying journeys are becoming shorter, more digital, and less telco‑centric, and differentiation is shifting away from features toward integration and enablement.

All this change is being accompanied with the ever-present issues of sovereignty and regulation. Data sovereignty, especially in the current geopolitical climate, is now a key topic of discussion among service providers. A fragmented European market only makes the challenge more pressing.

Service providers, however, need to have a pragmatic mindset, rather than an alarmist one.

SMBs don’t see sovereignty as a primary buying driver. The use of a large hyperscaler cloud is far more relevant to these smaller businesses, and sovereignty is materially relevant to only a handful of enterprises. If these businesses operate in a highly regulated environment like government or defence, data sovereignty is far more important to them.

The growing tension between emerging European guidance and existing frameworks, such as the US CLOUD Act of 2018, is also creating confusion. When operating across jurisdictions, providers must navigate between contradicting regulations.

So, what should service providers do? The key thing is not to over‑rotate on sovereignty as a sales message. They must understand which customer segments genuinely require it and design their propositions accordingly.

For anyone who attended this year’s Summit, they would already know that the most valuable insights always come from conversations throughout the day.

A recurring theme was how quickly global ambition exposes operational friction. Selling voice internationally involves far more than coverage, such as local licencing requirements and numbering regulations.

It’s something Gamma Communications has seen with the recent expansion into APAC. Providers, for example, must hold specific licences simply to issue local numbers. It’s both a cost and complexity burden that many service providers underestimate, until they attempt to scale.

This is exactly where global enablement models become commercially important. Those foundations allow service providers to extend reach without taking on disproportionate, unnecessary regulatory or operational risk.

Complexity around global regulations is giving service providers more to think about. In Singapore, for example, regulators are now getting tougher on sub-allocation and whether numbers are being provided without a licence. Providers need an SBO licence or at least work with a vendor that already has one.

Gamma’s own tri-party model in the APAC region helps to remove those obligations. What’s vital to remember is that no single provider can solve global communications alone. There are numerous factors providers need to consider when it comes to long-term growth.

Through strong partner ecosystems, shared operational responsibility, and models that allow international scalability, a foundation can be established. It reinforces a broader industry shift from transactional resale models towards a partnership that builds towards success.

The priorities service providers need to focus on all gravitate around building sustainable growth in 2026 and beyond. That can only be achieved by reducing friction for both partners and customers and avoiding any needless complexity.

Disruption will happen at the baseline – it’s never just a phase. If models are designed for platform-led buying, and there’s clear guidelines around sovereignty, then global growth will follow.

When a trusting partnership is combined with shared infrastructure, this becomes a reality rather than just another pipe dream.

If you’re ready to take your communications further, find out more about Gamma Communications’ service provider proposition.

Gas network company SGN confirmed it had repaired three minor gas leaks and left the site on Monday, August 3, six days earlier than expected.

The leaks were discovered during excavation works last month and contributed to the pushing back of the road’s reopening date, yet again, to September 20.

The completion of the gas mains replacement marked a significant step forward in the wider Oxford Station improvement project, which was originally budgeted at £161 million but is now expected to cost at least £237 million.

The development prompted hopes that Botley Road, closed beneath the rail bridge since April 2023, could reopen earlier than planned.

However, Network Rail has moved to manage expectations, saying the project remains on course to meet its existing target date rather than finish ahead of schedule.

A Network Rail spokesperson said: “We’re pleased that SGN has completed its gas mains replacement work.

“While this is an important milestone, it doesn’t necessarily mean the overall project will finish early as some remaining work is dependent on access to the railway, which we have had to rearrange to enable the replacement of the gas main.

“Our focus remains on meeting our planned deadline of 20 September for reopening Botley Road to traffic.”

While the completion of the gas works removes one of the most recent obstacles facing the scheme, Network Rail says further work under the bridge and around the station is still needed before the route can reopen to traffic.

The club is currently struggling in the summer heat, and has launched a new fundraiser to keep its gymnasts safe.

The club, which is based at Grove House Barn near Warkworth in Banbury, launched the fundraiser so it could buy and install four air conditioning units to keep its space cool.

Currently, the club hopes to raise £7,000 through the appeal so it can buy four 10kW air conditioning units and cover all the installation costs.

So far, the club has raised £380.

Karl Wade, director of Wade Gymnastics, said the club has become “increasingly warm” during the summer months due to the rising temperatures.

READ MORE: Thames Water leakage targets are ‘not realistic’ says boss after pay rise

“Despite our best efforts to keep doorways and shutters open, it becomes very uncomfortable for gymnasts to play and train,” Mr Wade said.

He added: “The safety of our gymnasts and coaches is always our utmost priority.

“Unfortunately, the risk of having to close the business during these hot spells is increasing and we need to have more effective ways of keeping everyone cool.

“An air conditioning system would allow the business to stay open during those extreme hot conditions and continue to provide classes for everyone who attends.”

The gym currently delivers classes seven days a week for around 900 people, which range from toddlers to athletes competing at national level.

The gym club was founded more than four decades ago by Ruth Wade and, for the past 20 years it has been based at its current facility.

SOFIAH NICHOLE SALIVIO

News Editor

Solihull Council has appointed ICS.AI to deliver the first phase of an AI Transformation Discovery programme to examine how artificial intelligence could be used across several resident-facing services.

The 24-week programme will review opportunities in Adult Social Care, Children’s Services, Economy & Infrastructure, and Public Health. It is intended to help the council decide where AI could be used and where future spending should be directed.

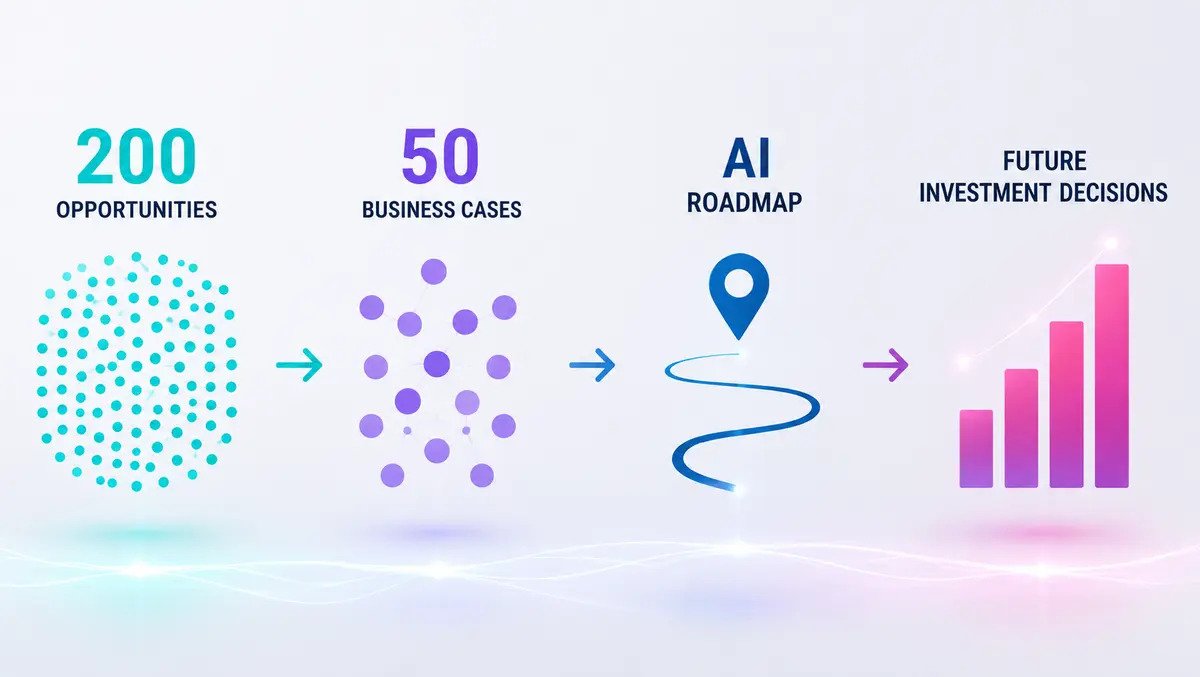

In this first phase, ICS.AI will assess the council’s readiness for AI and identify use cases across the four service areas. The programme is expected to produce a prioritised shortlist of about 200 use cases, including 50 validated from a finance perspective, alongside a longer-term AI Transformation Roadmap.

The work is intended to create an evidence base before any wider implementation decisions are taken. Ethics, privacy, and safeguarding will be considered throughout the assessment process.

Discovery phase

ICS.AI will use its AI Target Operating Model framework to review Solihull’s current position across five dimensions before ranking opportunities. The outputs will be based on council-owned baseline data and reviewed by public sector specialists.

The approach reflects a broader pattern among local authorities exploring AI in service delivery while facing pressure to justify spending and manage risks around data use and public accountability. Councils have also been seeking clearer business cases before committing to larger technology programmes.

Solihull said the discovery exercise would support a measured approach to service modernisation. The authority wants to identify where AI could improve services for residents while also demonstrating value for money.

“We are committed to taking a well-considered and planned approach to modernising the services we provide. By building a strong evidence base for future decisions, this programme will help us understand where the greatest AI opportunities exist. We will then be able to prioritise those improvements that will deliver the greatest benefit for residents, while ensuring full value for the council,” said Councillor Dave Pinwell, Cabinet Portfolio Holder for Resources, Solihull Council.

Public sector focus

ICS.AI said the Solihull engagement builds on work it has carried out with more than 20 public sector organisations using its AI transformation and discovery assessments. Those organisations include Derby City Council.

The company focuses on AI projects for the public sector, where interest has increased as authorities look for ways to manage demand pressures in social care, public health, and other frontline services. At the same time, councils are under scrutiny to show that new technology investments are proportionate and supported by practical evidence.

Dwayne Johnson, Chief Local Government Officer at ICS.AI, said local authorities need stronger justification before committing funds. “Local authorities need confidence that every investment is backed by robust evidence and long-term value for residents. Solihull Council is taking the right approach by starting with a structured discovery programme that builds a clear understanding of priorities before decisions are made. By developing finance-validated business cases and a practical roadmap, the council can be more proactive in the decisions it makes,” he said.

The programme’s initial outputs are expected to give Solihull a ranked view of where AI could be applied across services, the level of organisational readiness, and which projects may warrant further consideration. This first phase is focused on identifying options rather than moving directly into deployment.

For local government leaders, that distinction is becoming increasingly important as councils test AI in areas that affect vulnerable residents and essential public services. In Solihull’s case, the work spans some of the authority’s most visible functions, including care services, children’s provision, public health activity, and parts of local infrastructure planning.

The council aims to use the findings to inform later investment decisions through finance-validated business cases and a practical roadmap for future priorities.

-

Business & Technology3 weeks ago

Business & Technology3 weeks agoHSBC UK & Visa test AI shopping with live payments

-

Business & Technology3 weeks ago

Business & Technology3 weeks agoValarian lands USD $50 million backing for sovereign AI

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoMouser warns against viral hacks to cool overheating phones

-

Oxford News4 weeks ago

Oxford News4 weeks agoNew romantasy bookshop attracts queues of customers

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoSNP & Palantir launch AI tools for SAP transformations

-

Business & Technology4 weeks ago

Business & Technology4 weeks agoKane tops England influencer rankings after Mexico win

-

Traffic & Transport4 weeks ago

Traffic & Transport4 weeks ago‘I felt my spine and body split’: the woman who was hit by a child on a Lime bike – and denied compensation | Ebikes

-

Oxford News4 weeks ago

Oxford News4 weeks agoDWP now checking bank accounts for Universal Credit and Pension Credit